Postal Banking

By Mark Whitehouse, Bloomberg, Jan. 14 2016

Should the post office do more than handle the mail? Since the 19th century, governments around the world have used postal networks’ unparalleled reach to pursue a social goal: encouraging people, particularly the poor, to save money. But this venerable institution is in flux. Japan and China have begun to sell off chunks of their vast systems, while India is looking to expand its postal finance offerings. In the U.S., some Democrats want to revive the tradition to help the millions of Americans who lack access to reliable, reasonably priced financial services. Is postal banking an idea whose time has come or gone?

The Situation

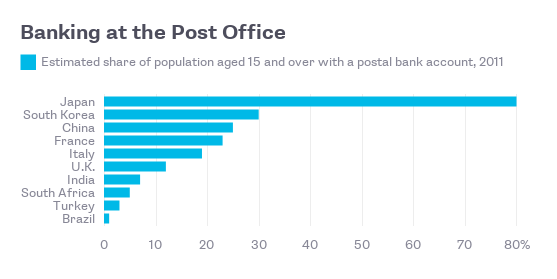

In November 2015, Japan sold an 11 percent stake in its postal service, which houses the country’s biggest bank by deposits and its largest insurer. The sprawling operations had become a symbol of government inefficiency and cronyism. It’s still required to deliver universal postal service, which is widely interpreted to mean it must maintain branches in rural areas. In December, China’s postal savings bank sold 17 percent of its shares to investors for $7 billion ahead of a planned public offering. The lender, which has 500 million customers and more than 40,000 outlets nationwide, wants the shareholders to help it offer investment banking and wealth management services and to expand and modernize its micro-finance lending, which is aimed at the country’s rural poor. India Post, the world’s largest mail delivery network, in January 2016 won permission to offer banking services, insurance products and delivery of government payments. In the U.S., prominent liberal politicians including Bernie Sanders, a Democratic presidential candidate, are pushing postal banking. They see it as a way to serve the unbanked while providing revenue to support the U.S. postal service’s network of more than 30,000 offices as mail delivery declines.

The Background

Great Britain created the first post office savings bank in 1861. The aim was to provide the working classes with a safe alternative to philanthropic and church-related institutions, which were inconvenient and sometimes corrupt. The innovation succeeded: Deposits flooded in, and by 1883 eight other countries — including France, Italy and Japan — had followed suit. One big exception was the U.S., where commercial banks were powerful enough to oppose postal banking. The system that ultimately emerged, in 1910, offered unattractive interest rates and funneled deposits primarily to those same commercial banks. After enjoying brief popularity during the Great Depression, the system fell into disuse and was abolished in 1966. Today, postal banks come in various forms. In the U.K., the Post Office doesn’t have its own bank, but does use its branches to offer a range of financial services from third-party providers such as Bank of Ireland and Aviva Life & Pensions. In France, by contrast, the national postal service has its own full-fledged financial institution, La Banque Postal.

The Argument

Proponents of postal banking point to a market failure: More than a quarter of U.S. households aren’t served by traditional banks, leaving them dependent on a patchwork of often predatory services such as payday and auto-title lenders. The answer, they say, is for a government, or quasi-government, entity to step in. Officials in India say the trust built up over the postal service’s more than 200-year history can help it lure potential savers who are wary of banks, and that society as a whole will benefit from the capital they help accumulate. The track record of postal banking suggests a trade-off. Government-run postal banks can be effective in reaching rural and other underserved populations, but can also be used to divert savings to investments whose goals are more political than profitable. Opponents of postal banking argue that getting the unwieldy postal bureaucracy involved in financial services can be a disaster that could stifle startups working to adapt mobile technology and new data tools to serve the unbanked. Still others think a third way might lie in the combination of new online or prepaid services and the kind of partnership long used in the U.K.

THE REFERENCE SHELF

A report on postal banking from the United States Postal Service Office of the Inspector General. And another.

A book by economic historian Sheldon Garon that focuses on postal banking as a vehicle for promoting savings.

A book by legal scholar Mehrsa Baradaran on postal banking and financial inclusion in the U.S.

A Bloomberg article on the potential for postal banking in the U.S. And another.

A UN report on postal banking and financial inclusion for women, and a World Bank study analyzing the characteristics of postal banking customers.